MARKETSCOPE : AI or Crash… ?

July, 15 2024

We shall not embark on an attempt at dispassionate analysis of what the appalling happening in Butler, Pennsylvania, will mean for markets and the economy. The bottom line is that the chance of an eventual Trump victory is greater.

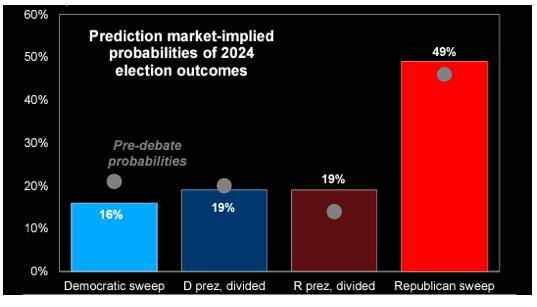

These were the prediction market odds of a clean Republican sweep BEFORE the assassination attempt.

Either traders don’t think it’s worth pricing in a Trump victory yet, or they don’t think he would be that bad for the bond market.

Another reason not to expect a drastic reaction is that, to quote Roche: “The markets have developed a great immunity to worsening geopolitical news… I do not remember the disconnect being greater. The markets don’t give a toss about worsening war in Ukraine or French collapse into ungovernability!”

The last few years appear to show that geopolitics doesn’t move share prices; investors may be over-applying it.

Now let’s resume our market review.

Wall Street’s benchmark S&P 500 index posted a two-week win streak on Friday. Its torrid run has seen it notching gains in 10 out of 12 weeks dating back to the end of April. Remarks by Federal Reserve chair Jerome Powell on Capitol Hill hinting at interest rate cuts, and a June consumer price index report that came in softer than expected, US inflation is easing, US CPI headline prices fell 0.1% in June, the first decline in 4 years, which should lead to a first rate cut in September, were the primary drivers of last week’s advance.

The biggest advance was notched by the small-cap Russell 2000 Index, which gained 6.00%, marking its best week since early November. Value stocks also handily outperformed growth stocks.

The Euro STOXX 600 Index ended the week 1.45% higher while Japan’s TOPIX index hit a record high on Thursday, over 40’000.

AHEAD

The Fed will still garner some attention as traders will be keen to hear from a jam-packed slate of central bank speakers, just ahead of the pre-monetary policy meeting blackout period. We’re expecting Chinese GDP and retail sales on Monday, the German ZEW index for July.

The spotlight this week will shift somewhat to the second quarter earnings season from the Federal Reserve and monetary policy. Market watchers will receive results from several major names, including Dow 30 components Goldman Sachs, UnitedHealth, Johnson & Johnson and American Express, along with streaming giant Netflix.

SEE EARNINGS trend below

MARKETS : Sellers Live Higher. Buyers Live Lower.

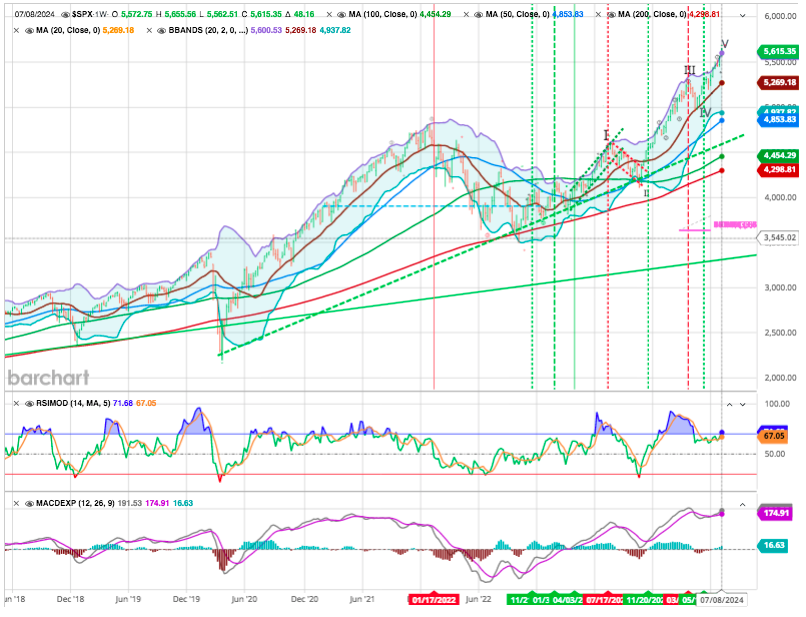

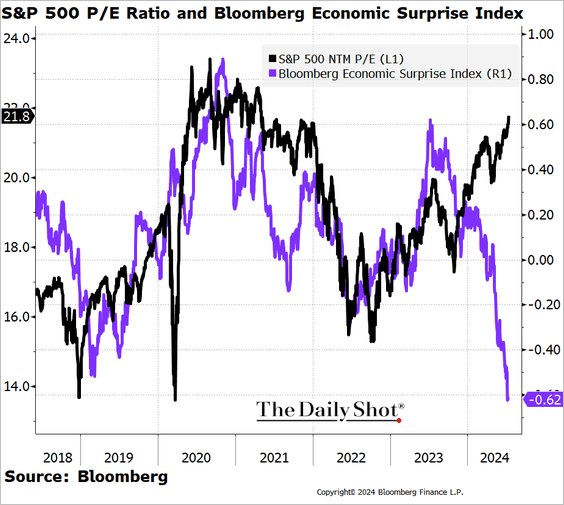

The markets continue in one of the most extended rallies on record. S&P 500 technically overextended and fundamentally overvalued, facing rare conditions that historically signal caution.

The “greed factor” has overtaken logic in the current market environment. . During strongly trending bullish markets, investors become overconfident in pursuing gains as “greed” overtakes “logic.” Such is the basis of the psychological behaviors that repeatedly lead to poor investor outcomes.

The S&P 500 has hit multiple extremes that scream danger. This index is technically overextended and fundamentally overvalued but close to a breaking point. Much of this has been driven by investors piling into a handful of names, while more recently, a volatility dispersion trade has pushed correlations beyond historical extremes, which is due to unwind as earnings season moves into a higher gear.

The S&P 500 is technically stretched, with the relative strength index over 70 on the weekly chart, while also trading above its upper Bollinger band. The two conditions, when combined, have only flashed overbought readings simultaneously five times since 2018, and four of those five times saw sharp pullbacks in the index. The other time, the index traded sideways for several weeks.

The market did indeed flip last “sell signal,” pushing higher and topping 5600 for the first time. However, it also pushed the market back into extremely overbought territory, and the deviation from the 50-DMA is quite significant.

Such suggests that, as we saw in late May and June, the market will either consolidate or correct back to the 20-DMA. If the bulls can hold that level again, as they have, the market could continue to push higher. Such is possible given the current exuberance surrounding the Fed cutting rates.

However, if the 20-DMA fails, as in early April, the 50-DMA becomes the next logical support, with the 100-DMA close behind. Such would encompass another 3-5% correction.

While the bulls are very confident, the risk of a 5% to 10% correction over the next three months remains elevated.

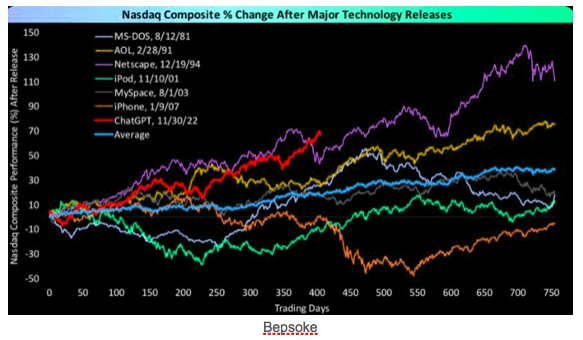

The Nasdaq post-ChatGPT at just over 400 days is now up more than it was following any of the other major technological releases of the last half-century. But if we are to follow the Netscape blueprint we have a lot of more bull left…

Since the start of 2023, 97% of NVDA’s return has been driven by greater earnings (vs. just 3% from valuation expansion). However, year to date, NVDA’s NTM P/E ratio has increased from 25x to 42x (+70%), accounting for 56% of the 165% YTD price return.

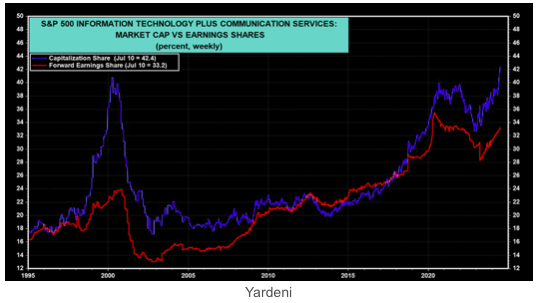

The market capitalization of S&P 500 Information Technology and Communication Services sectors has melted up to 42.4% of the S&P 500, exceeding the 40.7% peak during March 2000.

Also keep in mind that the stock market might be overlooking signs of a softening US economy.

Japan’s Nikkei hits record high on tech gains and foreign buying

The Nikkei 225 index was the best performer in Asiato a record high of 41,421.50 points. The broader TOPIX index rose 0.4% and was in sight of a record high hit last week.

Expectations of major corporate reforms in Japanese companies, which are expected to see them prioritize shareholder returns, also made local markets appear more attractive.

Technology stocks, especially chipmakers, were the biggest boost to the Nikkei, as they tracked gains in their U.S. peers on hype over artificial intelligence.

Weakness in the yen, which was near a 38-year low, also boosted export stocks.

Chinese stocks lag on trade jitters

China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes recovered a little dragging Hong Kong’s Hang Seng.

Sentiment towards China remained strained after the European Union imposed steep tariffs on the import of Chinese electric vehicles. Markets were watching for any retaliation from Beijing, especially as officials flagged the possibility of a trade war over the tariffs.

Chinese stocks largely lagged their peers through June as optimism over an economic rebound in the country wore thin amid middling economic readings. Focus this week is on trade and inflation readings from China for more cues on the country.

China’s economy, which remains bifurcated between strength in exports and manufacturing activity and weakness in housing and credit, coupled with very low inflation

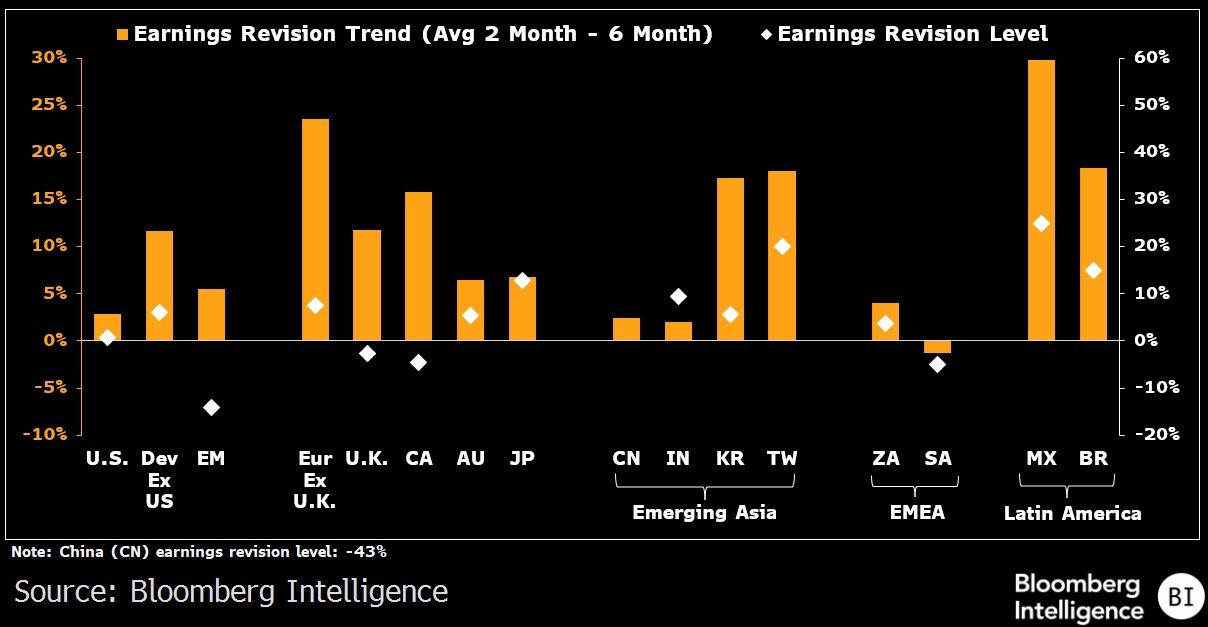

EPS growth projections are trending up across regions

Revisions are picking up outside of the U.S.

Forward estimate revision momentum is improving across 13 of the 14 major markets we track globally, with the lone exception of Saudi Arabia, led by Europe among developed markets and emerging nations in Latin America and Asia. Developed markets are outpacing US revision momentum even though UK and Canadian revisions are still negative.

Mexico and Taiwan have the strongest revision scores among major markets, and positive shifts in Brazil and South Korea are also helping offset major revision weakness that persists in China. Even China has shown some minor improvement in revision trends as the last two months were better than the prior six. Revision levels are defined as the number of forward 12-month EPS analyst upgrades and downgrades as a percentage of total revisions.

Stocks outside the US may be the primary beneficiaries of improving risk tolerance if the Federal Reserve engineers a soft landing with a policy reversal in 2H.

While US stocks, particularly mega caps, helped power global equities to new highs in the first half, stocks elsewhere struggled to keep up. The Bloomberg World Index is now more than 8% above its 2021 high while non-US stocks remain 5% below their peak — leaving room for a catch-up trade to emerge if risk tolerance improves with lower rates.

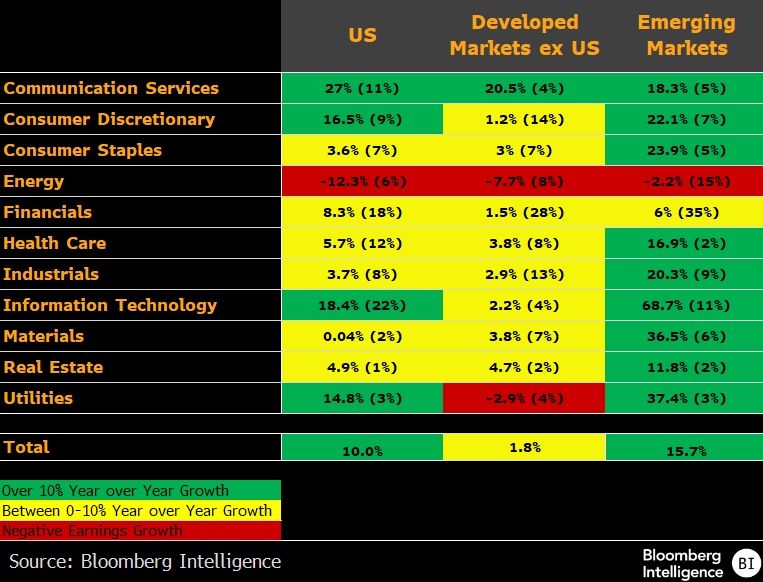

Heading into 2Q earnings season, consensus anticipates that US and emerging markets will report double-digit earnings growth this year.

That contrasts with the other developed markets, which should lag well behind because of their smaller and weaker tech sectors. Earnings should grow in some developed markets, just 0.4% in the euro zone, 5.9% in Canada and 7.6% in Japan. Yet UK and Australian earnings are expected to contract, led by declines in their financial sectors.

Within emerging markets, only energy is expected to post lower earnings in 2024 than in 2023, with all other sectors except for financials poised for double-digit growth.

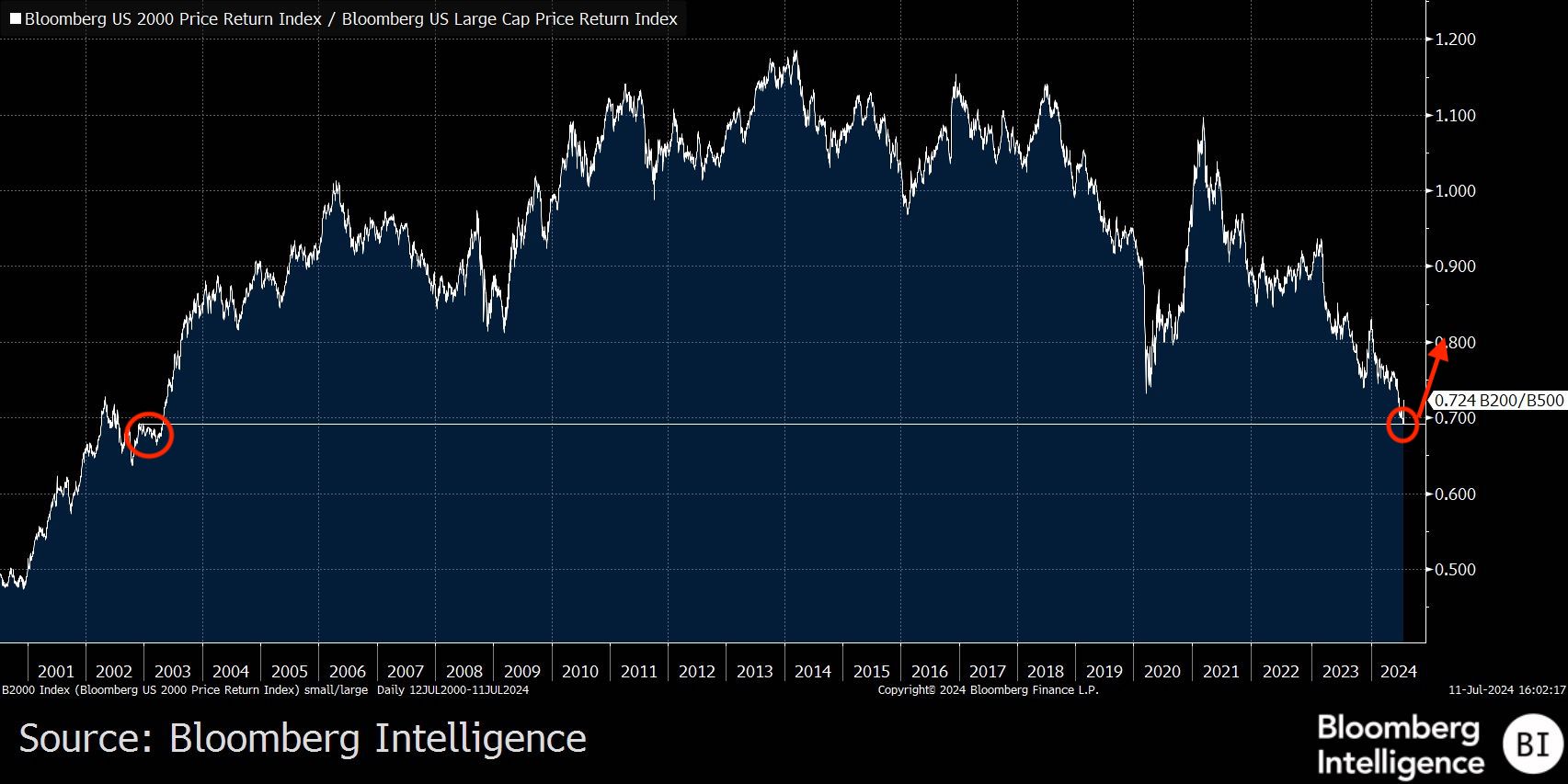

Time to buy small-cap stocks?

US Small-caps Russell 2000 just posted their widest margin of outperformance over large-cap tech at the exact level where this ratio bottomed (and stocks peaked) in March of 2000… Is it the start of a new cycle of outperformance for small caps?

Russell 2000 vs large cap.

The earnings cycle is turning in support of a catch-up trade for non-mega-cap stocks, and the possibility of the Federal Reserve easing interest rates in September might be the spark needed for the 493 and small caps to stage a 2H rebound.

On July 11, Small caps had their third-strongest gain relative to large caps since 2000. Other surges of similar size started recovery rallies in October 2011 and March 2020.

Small caps jumped 3.5% on July 11, outperforming large caps by 4.4% in their biggest single-day relative gain since 2008 and greatest absolute increase since November as easing CPI sparked hopes a Fed cut is coming. The one-day surge may bode well for gains to extend. Since 2000, there were eight times where small caps outgained large caps by more than 300 bps. In the month following those instances, small and large caps gained 8% and 6.5%, respectively.

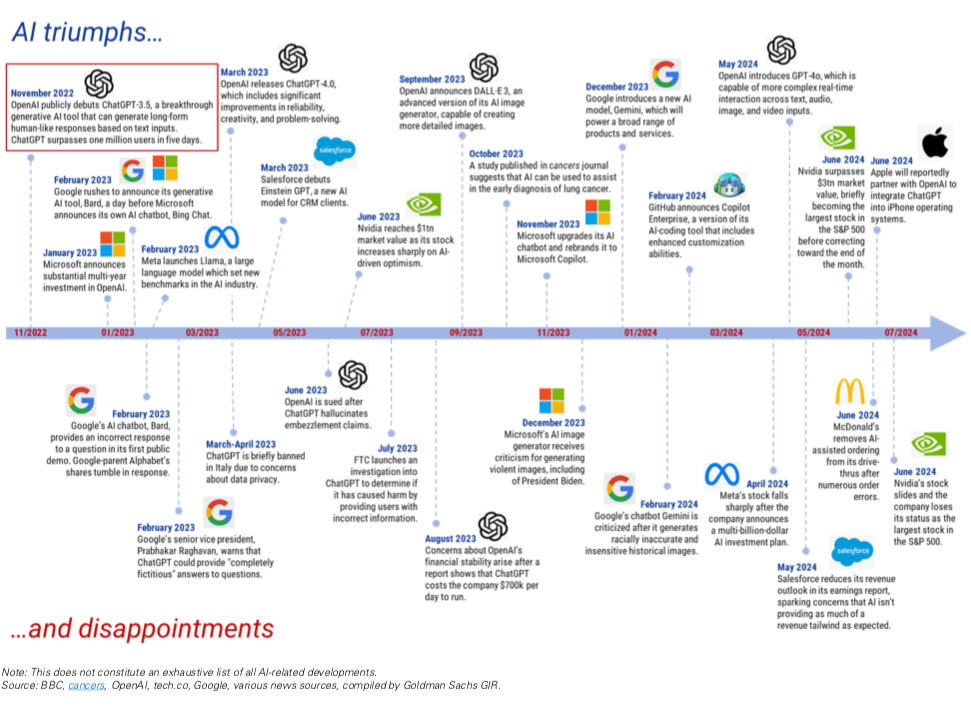

AI TRANSITION : Too Much Spend, Too Little Benefit ?

Check Goldman Sachs report here

Eighteen months after the introduction of generative AI to the world, not one truly transformative—let alone cost-effective—application has been found. Over-building things the world doesn’t have use for, or is not ready for, typically ends badly.

Question : Are you just concerned about the cost of AI technology, or are you also skeptical about its ultimate transformative potential?

Jim Covello: I’m skeptical about both. Many people seem to believe that AI will be the most important technological invention of their lifetime, but I don’t agree given the extent to which the internet, cell phones, and laptops have fundamentally transformed our daily lives, enabling us to do things never before possible, like make calls, compute and shop from anywhere.

Currently, AI has shown the most promise in making existing processes—like coding—more efficient, although estimates of even these efficiency improvements have declined, and the cost of utilizing the technology to solve tasks is much higher than existing methods. For example, we’ve found that AI can update historical data in our company models more quickly than doing so manually, but at six times the cost.

More broadly, people generally substantially overestimate what the technology is capable of today. In our experience, even basic summarization tasks often yield illegible and nonsensical results. This is not a matter of just some tweaks being required here and there; despite its expensive price tag, the technology is nowhere near where it needs to be in order to be useful for even such basic tasks.

And I struggle to believe that the technology will ever achieve the cognitive reasoning required to substantially augment or replace human interactions. Humans add the most value to complex tasks by identifying and understanding outliers and nuance in a way that it is difficult to imagine a model trained on historical data would ever be able to do.

Happy trades

The current investment environment shares some similarities with that of the Internet Bubble, a period that we remember well as a money manager.

We use our experience and lessons learned to offer a strategy to protect profits in a speculative market.

check